ICSE Class 10 Maths GST Notes (OP Malhotra) 2026-27. We Provide Step by Step Answer of all the exercises with Chapter Test of S Chand OP Malhotra Maths . Visit official Website CISCE for detail information about ICSE Board Class-10.

ICSE Class 10 Maths GST Notes (OP Malhotra) 2026-27

Introduction

Every government be it central or state government needs money for administrative expenses , welfare and development schemes , salaries and employees.

Government collects money by levying taxes within their respective territories.

Earlier, there were multiple indirect taxes like VAT, Excise Duty, and Service Tax.

To simplify the system, GST was introduced as a unified tax system.

What is GST?

GST (Goods and Services Tax) is an indirect tax applied on the supply of goods and services.

- Replaces multiple taxes

- Applied at every stage of sale

- Charged only on value addition

- Final burden on consumer

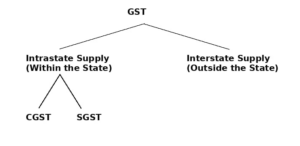

Types of GST

GST too needs to have clear provisions on what ares the centre and state government are allowed to collect revenue to prevent oberlapping.

- CGST: (Central GST) Collected by Central Government

- SGST: (State GST) Collected by State Government

- IGST: (Integrated GST) Charged on inter-state transactions

| Transaction Type | Tax Applied |

|---|---|

| Within State | CGST + SGST |

| Between States | IGST |

GST Rates

- 0% (Essential goods)

- 5%

- 12%

- 18%

- 28%

GST vs VAT

| GST | VAT |

|---|---|

| Based on value addition | Based on total value |

| Uniform across India | Different in each state |

| Transparent system | Less transparent |

More about GST

- A consumer (end user) cannot claim the GST paid by him.

- Only a person or an organization registered with GST can charge and collect GST on sale/transfer of goods and services.

- Anyone who charges GST has to mention the GST registration number on the bill.

- GST is applicable on every type of movement of goods/services.

- Integrated GST (IGST) is for movement of goods within the states of India . This is collected by the centre but is transferred over to states.

- Inter-state means : supply from one state to another state. However, the central government later distributes IGST between the respective state governments as per laws.

- In case of intra-state transaction, the seller collects both CGST and SGST form the buyer and deposits the CGST with the central government and the SGST with the state government.

- GST is calculated on sale price obtained after deducting discount, if any from the list price.

- In case of intra-state sale of goods/services or both If GST rate is 18% then CGST 9% of sale price, SGST 9% of sale price, IGST = 0

- In case of inter-state sale of goods or services or both If GST rate is 18% then IGST 18% of sale price

- Discount is never allowed on amount including GST.

Input GST and Output GST

- Output GST: Tax collected on sales

- Input GST: Tax paid on purchases

Formula for calculating GST:

- GST Payable = Output GST – Input GST (if Output GST is more than Input GST)

- GST Credit = No GST to be paid (if Input GST is more than Output GST)

Input Tax Credit (ITC)

Input tax credit means that while paying tax on sale (output) of goods and services you can avail the tax you have already paid on the purchase (input) of the above goods/services and pay only the balance amount as tax.

Input-tax credit can be availed only on goods/services for business purposes.

NOTE:

- Input tax includes CGST/SGST/IGST paid on input goods, input services, etc.

- Only a registered person is entitled to take credit of input tax charged on supply of goods/services.

- Credit of tax paid on every input used for supply of taxable goods or services or both is allowed under GST

- For the purchase of petroleum products, liquor, petrol, diesel, motor spirit, etc input tax credit is not available.

- In exports of goods/services, GST is not payable, but still input tax credit is available. Such transactions are called zero-rated transactions in GST.

Important Terms:

Dealer : A person who buys godds or services for re-sale.

Cost Price : It is the price at which goods are purchased.

List Price : Price at which an article is marked . It is also known as marked/printed/quoted price.

Selling Price : It is the price at which a trader sells his goods with discount.

Selling Price = List Price – Dicount = Discounted Price

Formulas

- Total GST = CGST + SGST

- Final Price = Cost Price + Total GST

- GST Amount = (GST rate × Taxable Amount)/100

Example :

If the cost price of a product is 1000 rupee and GST is 18% , then :

GST Amount = 18×1000/100 = 180

Final Price = 1000 + 180 = 1180

Important Points

- GST is charged on value addition only

- Input tax credit avoids double taxation

- GST is applied after discount

- CGST + SGST for intra-state

- IGST for inter-state

So , this was ICSE Class 10 Maths GST Chapter 1 Notes (OP Malhotra) .

Now you should solve some practice problems.

Practice Questions on GST :- Exe-1

— : End of ICSE Class 10 Maths GST Chapter 1 Notes :–

Return to :– OP Malhotra S Chand Solutions for ICSE Class-10 Maths

Thanks

Please Share with Your Friends